Ironic Quirks

I’m going to highlight a rather ironic quirk about GLP-1s that no one else is talking about.

And it’s directly applicable to the apparel supply chain.

Our thesis is that the issues of fit, size, returns and excess inventory are being incorrectly assigned to GLP-1s. The drugs aren’t the cause. They’re a magnifying glass, exposing the fragility of the apparel supply chain and the processes that underpin it; this is a fundamental principle of Fit VolatilityTM.

The catch-all of “weight loss” isn’t the real issue. It’s the pace and direction of body composition change, fat-to-lean-mass ratios, for example. And if someone discontinues the drug, the rate of regain and the composition shift that comes with it.

Here’s the curious part. Eli Lilly recently reported the most powerful weight-loss results from any novel therapeutic to date. Its next-generation shot, retatrutide, helped patients in a clinical trial lose 30% of their body weight over two years, exceeding what’s on the market today like Zepbound and Wegovy.

Retatrutide isn’t approved yet. It’s awaiting the FDA, with market entry expected in 2027.

Oddly enough, Ken Custer, President of Lilly’s Cardiometabolic Health unit, said the company will need to move away from a “one size fits all” approach in the coming years. In his view, it’s unreasonable to assume everyone will be satisfied with a single medicine.

Two Threads

There are two threads to pull on here for apparel.

First, the demand side. Retatrutide amplifies the magnitude of weight loss. But the quality of that loss is still in question, and so is whether people will stay on it long term. So what does that mean for apparel returns, fit issues and excess inventory?

The caveat: every brand needs to think hard about how much of its ideal customer base will actually adopt GLP-1s. A minority is one thing. A majority is a problem.

The second thread is where the irony lives. Why is Eli Lilly the one setting the pace on weight loss while competitors like Boehringer Ingelheim struggle?

The answer is process innovation.

And for that, we rewind to 2023, and my favorite WSJ article ever. The subject was Eli Lilly’s pending launch of Mounjaro, touted at the time as the “King Kong of Weight Loss Drugs.”

What mattered wasn’t the scientific breakthrough. It was how a pharma company, working with complex products and long lead times, unwound its own organizational dysfunction to get Mounjaro to market fast and compete with Ozempic.

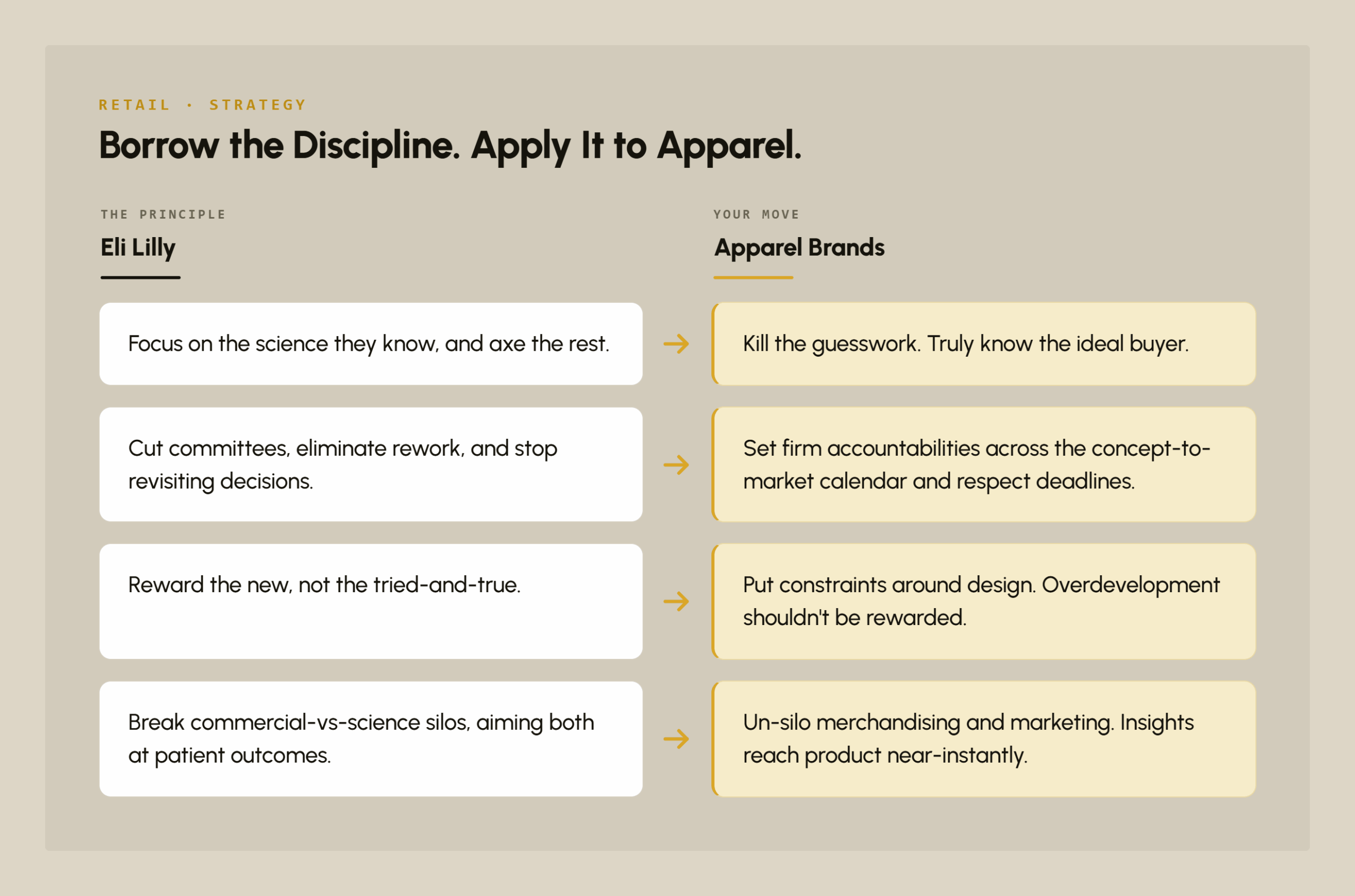

More specifically, Lilly did the following:

1 – Doubled down on the science they knew well. Everything else got axed.

2 – Eliminated committees and the bureaucracy around decision-making, including the habit of revisiting settled decisions.

3 – Rewrote business-unit incentives so teams were rewarded for selling novel. therapeutics, not defending the tried-and-true to protect their metrics and bonuses.

4 – Smashed the silos between commercial teams and scientists, pointing both at patient outcomes.

The irony: process innovation is what let Lilly bring novel GLP-1 drugs to market faster and set the pace on weight loss, a pace that will ripple into every consumer-facing industry, especially apparel.

And if any industry needs process innovation, it’s apparel!

Think about it. Read those four actions translated into the language of apparel:

1 – Eliminate guesswork in planning and truly understand who the ideal buyer is.

2 – Set firm accountabilities in the concept-to-market calendar and respect deadlines.

3 – Put constraints around design. Overdevelopment shouldn’t be rewarded. Being incentivized to be creative isn’t a blank check the rest of the organization pays for.

4 – Merchandising and marketing aren’t siloed from one another. Insights flow to product creation with near-zero lead time.

The bottom line: if process innovation is good enough for the most complex products, it’s good enough for the pants you’re shifting in right now. Quince’s $10B valuation didn’t come from nowhere. It’s the product of superior process.

For apparel brands, investing in process now will prove a felicitous choice.

Eventually, the impacts of GLP-1s will stabilize.

But will the apparel supply chain still be as fragile as it is today?